Programmatic Video Private Exchange Use In U.S. Surges Another 140%

- by Tyler Loechner @mp_tyler, September 5, 2014

The amount of pre-roll video inventory available for programmatic buying increased 14% from Q1 to Q2 2014, and much of that growth was driven by high-end publishers getting on board with programmatic selling.

The data comes from TubeMogul’s Q2 2014 quarterly update on the U.S. digital video ad marketplace.

Per TubeMogul’s report, the amount of inventory available for real-time bidding (RTB) from “Tier” 1 publishers and comScore Top 100 sites increased by 48% and 65%, respectively. That’s down from the respective growth figures of 110% and 78% posted in between Q4 2013 and Q1 2014 -- but it still represents a clear upward trend.

Private marketplace use continues to surge, with 140% more advertisers buying inventory directly from publishers via TubeMogul’s BrandAccess (its private marketplace service). The use of BrandAccess has grown 1,500% since Q4 2013, which TubeMogul calls “astonishing.”

Another area of exceptional growth is mobile video. TubeMogul says the amount of mobile video available for programmatic buying in the U.S. has increased by over

1,000% in the past nine months, attributing the growth to “the addition of several major exchanges.”

A TubeMogul representative acknowledged that the addition of mobile inventory sources skews the numbers, and that “while [TubeMogul] did enjoy some growth, it’s not 100% representative,” adding that it should “stabilize next quarter.”

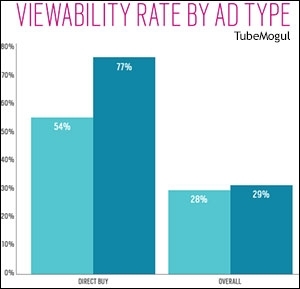

While viewability rates for inventory purchased direct from publishers increased 39% (up to 77%) quarter-over-quarter, TubeMogul notes that the overall viewability rates were nearly identical to Q1 2014 -- checking in at an abysmal 30%, just 1% better than the previous quarter.

The lack of overall improvement on the viewability front was highlighted in a report form video ad management firm Vindico earlier this week. How the Media Rating Council (MRC) now-implemented standard of “50% of the video ad being in-view for at least two seconds” changes the pictures remains to be seen.

The cost to buy pre-roll video inventory increased 13% quarter-over-quarter, with all types of inventory -- from “premium” to “remnant” -- becoming at least 10% more expensive in Q2.